7 Blockchain Challenges to be Solved before Large-Scale Deployment

When organisations adopt new technologies, the context of that technology plays an important role. How people deal with the material properties of new technology is informed by their previous experience of using or not using similar technologies in the past. Since blockchain is still a new technology, how organisations adopt this technology also depends on how existing and related challenges are resolved. These affect how organisations apply blockchain and smart contracts, and whether the design and decision-making capabilities within will or can change at short notice.

Currently, many enterprises are experimenting with blockchain, but few have implemented a decentralised solution. According to a 2019 Deloitte report on enterprise blockchain adoption, 53% of the 1386 interviewed executives stated that blockchain had become a critical priority. However, only 23 per cent have actually initiated a blockchain deployment. While blockchain is gaining traction and acceptance in more industries, there are still some challenges left that need to be fixed first before we will see large-scale deployment. Let take a look a seven blockchain challenges that need to be fixed;

Seven Blockchain Challenges

1. Scalability

The first challenge is the technical scalability of blockchain, which is, at least for public blockchains, a hurdle that could limit their adoption. For example, the bitcoin blockchain is growing at 1 MB per block every ten minutes and currently has a size of 241 GB, while an Ethereum full archive node currently takes up over three terabytes of data. Nodes that want to validate transactions are required to download the entire bitcoin blockchain, which could pose a problem in the long run. Of course, there are plenty of other blockchains that take a different approach and, maybe require less storage. However, growth in data coming our way – 175 zettabytes per year in 2025 – this could become problematic.

Scalability is less of a problem for private blockchains, such as Hyperledger, since the nodes in the network have a direct interest in processing transactions; this means the computational power required to validate blocks is less of an issue. If transactions cannot be verified in real-time or within a short time frame, this affects the technical adoption of a blockchain, as rapid decisions are often required, especially in today’s high-velocity environments.

2. Transaction speed

The second challenge is related to the transaction speed of a blockchain. In 2019, the bitcoin blockchain is still capable of only processing seven transactions a second, while the Ethereum blockchain could, theoretically, process eight. However, at the 2018 Singles’ day in China, Alibaba processed 325.000 transactions per second (resulting in a revenue of $30.8 billion in 24 hours). Blockchain will take time to reach these levels. Meanwhile, new distributed ledger technologies are being developed that offer thousands or even millions of transactions each second. However, the deployment of these new distributed ledger technologies in enterprise environments is still limited.

3. Decentralisation

The third challenge involves the level of decentralisation with the bitcoin blockchain. Although this does not apply to all distributed ledger technologies, it is important to emphasise. The power of Bitcoin lies in the fact that it was designed to be decentralised, in that not one centralised stakeholder could control the network. However, today’s mining pools nonetheless control a majority of Bitcoin’s collective hash rate. Six mining pools together control over 75% of the mining power. This centralisation of validating transactions is a logical consequence of how the bitcoin protocol was developed, as it rewards economies of scale. This does not have to be a problem, as long as the mining pools can be trusted and have an incentive to do the right thing.

Of course, decentralisation is tackled differently when it comes to private blockchains. Since everyone is known in the network, it does not matter if only a dozen nodes control the network. However, when a company such as Facebook aims to develop a global cryptocurrency Libra using a private network, with a maximum of 100 players to begin with, this can be considered problematic. Only fully decentralised blockchains are tamper- and censorship-resistant and so far, there are only limited examples of truly decentralised blockchains.

4. Lack of Talent

The fourth challenge, from an organisation design perspective, is the lack of talent to build decentralised applications. Educating employees to work with blockchain takes time; however, it is not yet taught at many educational institutions. Only 50% of the world’s top universities offer a blockchain course. As is the case with all new technologies, organisations and academia need to work together to ensure the correct curriculum is introduced.

There are already hundreds of blockchain start-ups, all trying to attract the same limited talent, yet organisations are faced with a talent pool that is expanding more slowly than demand is growing. Therefore, organisations that want to embrace blockchain technology need to have deep pockets to pay for expert salaries or rely on employees that have only just started learning this new technology.

5. The Ecosystem

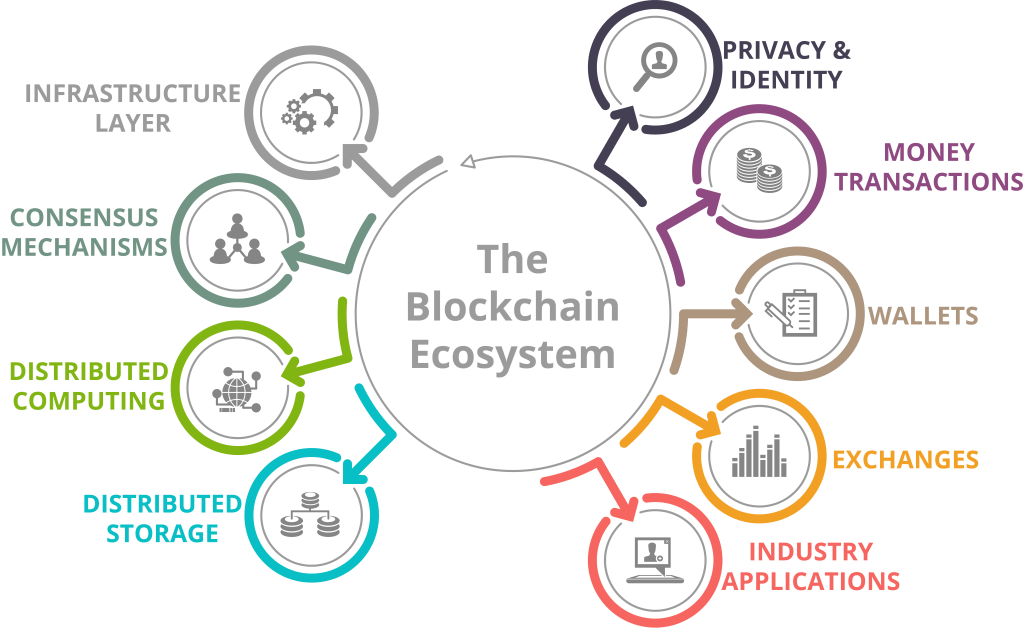

The fifth challenge is that a decentralised ecosystem surrounding blockchain and supporting distributed products and services is needed. This includes decentralised cloud storage (currently being developed by companies such as Ethereum and the InterPlanetary File System), decentralised archiving, decentralised communication and decentralised domain name servers. Most of these technologies are not yet fully developed, resulting in significant risks for anyone who wants to get involved with blockchain and develop completely decentralised and autonomous organisations. However, the decentralised ecosystem consists of multiple layers, which many of these layers are still under development:

- Infrastructure layer: those applications that aim to create an infrastructure layer on which others can develop applications. Public blockchains include Ethereum, EOS and Nxt, while private blockchains include Ripple, Hyperledger, MultiChain and Chain.

- Consensus Mechanisms: Required to ensure the state of the network and to determine which node can validate transactions. There are numerous consensus algorithms available, ranging from Proof of Work (PoW), Proof of Stake and many others.

- Distributed computing: using distributed ledger technology to distribute your computing requirements. Basically, cloud computing but then decentralised. Examples include Golem and Sonem.

- Distributed storage: distributed data storage is especially important when you want to be sure that data can always be accessed, regardless of restrictions some countries have. Examples include Storj, IFPD and FileCoin.

- Privacy & Identity: Services that are focused on developing a self-sovereign identity and ensuring that data of internet users is kept private and personal. Examples include Sovrin, uPort, Civic and Blockstack.

- Money transactions: As discussed in Chapter 4, there are four different types of tokens: currency, security, utility or asset tokens. Currency tokens, meaning cryptocurrencies, are used to make financial transactions, and the most well-known is, of course, Bitcoin. Others include ZCash, Bitcoin Cash or Monero.

- Wallets: Of course, all those cryptocurrencies need to be kept somewhere. Wallets are the bank accounts of the crypto world. You can have hot wallets (connected to the internet) or cold wallets (disconnected from the internet). Examples include MyEtherWallet, Jaxx, Exodus or Trezor.

- Exchanges: Like with stocks in companies, tokens need to be exchanged, so there is a range of centralised and decentralised exchanges. Centralised exchanges have the risk of being hacked, which is not possible with a decentralised exchange. Examples of centralised exchanges include Bitfinex, Bitstamp, Coinbase or Kraken. Examples of decentralised exchanges include 0x, bisq, bitshares or EtherDelta.

- Industry applications: Every industry can use DLT to improve collaboration, enable provenance, speed up transaction settlements or enable transparency.

6. Energy consumption

The sixth challenge concerns the energy consumption of decentralised networks. Although there are a variety of consensus mechanisms, the Proof of Work consensus mechanism is still the most used. PoW requires solving complicated puzzles, which uses vast amounts of energy. It is estimated that the PoW consensus mechanism in the bitcoin blockchain currently consumes 66.7 terawatt-hours per year, which is comparable to the total energy consumption of the Czech Republic, a country of 10.6 million people.

Fortunately, new blockchains might use different consensus mechanisms, which require significantly less energy. In recent years, the number of available consensus algorithms has exploded. It seems that every blockchain is developing its own consensus mechanism. Here is an overview of what is out there:

- Delegated Proof-of-Stake: same as Proof of Stake, but the number of tokens you own determines who gets to vote and elect witnesses;

- Leased Proof-Of-Stake: users can develop their own tokens, which they can use to improve their security on their server farms;

- Proof of Elapsed Time: similar to a Proof of Work algorithm, but the difference is that this algorithm focuses more on the duration of the computation;

- Simplified Byzantine Fault Tolerance: there is one validator that can bundle multiple transactions to create a new block;

- Delegated Byzantine Fault Tolerance: this consensus mechanism uses game theory to verify blocks among professional miners;

- Directed Acyclic Graphs: they do not have a blockchain structure, but often require users to validate two transactions if they wish to add one transaction. This verification can use a simplified Proof of Work algorithm;

- Proof-of-Activity: a combination of Proof of Work and Proof of Stake to make sure that tokens offered as a reward are on time;

- Proof-of-Importance: the more you send and receive transactions on the blockchain, the more tokens you will receive;

- Proof-of-Capacity: used especially for decentralised storage as it utilises the availability and capacity of storage space on a user’s drive;

- Proof-of-Burn: miners have to show proof that they burned tokens, which means sending them to verifiable unspendable addresses;

- Proof-of-Weight: similar to Proof of Stake, but it depends on various other variables, called ‘weights’, which basically means combining various features of various consensus algorithms.

7. Resilience, irreversibility, quantum computing and lack of standards

There are also challenges related to data on a blockchain. Resilience and irreversibility are two key attributes of blockchains; once data or transactions are appended and accepted by a network, they can no longer be changed. However, only authenticity can be ensured through a blockchain, not reliability and accuracy. If bad data are offered correctly, they will end up on a blockchain; likewise, if a document contains false information but is offered right, it will end up on a blockchain.

Theoretically, data on a blockchain will be there indefinitely, but the development of quantum computing means the cryptography used today might not be secure in the (near) future. Therefore, data governance will only increase in importance within organisations adopting blockchain. Poor execution of smart contracts and, hence, poor automated decision-making, can subsequently result in tremendous problems.

Although blockchain reduces costs and increases efficiencies due to a shared ledger and smart contracts, lack of standards could cause a counter effect. Standards are important for networks that deal with information systems, and they can help to align an industry. However, obtaining global industry standards for new IT is difficult, and it could take some time before organisations have a shared global blockchain standard, on which the International Organization for Standardisation is currently working.

Final Thoughts

Blockchain is a promising technology. Blockchain, particularly when used in concert with other technologies, offers organisations an opportunity to re-think their internal and external processes, remove inefficiencies, improve transparency and provenance and build a better organisation overall. However, it faces numerous challenges that could affect its adoption across organisations. However, significantly more research is required to overcome the considerable governance and technological challenges involved therein.

Scalability and a lack of speed, talent and standards could slow down both its implementation and the development of new blockchain applications, negatively affecting the development of new organisational forms such as decentralised autonomous organisations. Yet, despite these challenges, there have been dozens of new applications in almost every industry that apply distributed ledger technologies and are already benefit from this fundamental technology.

Dr Mark van Rijmenam

Dr. Mark van Rijmenam, widely known as The Digital Speaker, isn’t just a #1-ranked global futurist; he’s an Architect of Tomorrow who fuses visionary ideas with real-world ROI. As a global keynote speaker, Global Speaking Fellow, recognized Global Guru Futurist, and 5-time author, he ignites Fortune 500 leaders and governments worldwide to harness emerging tech for tangible growth.

Recognized by Salesforce as one of 16 must-know AI influencers , Dr. Mark brings a balanced, optimistic-dystopian edge to his insights—pushing boundaries without losing sight of ethical innovation. From pioneering the use of a digital twin to spearheading his next-gen media platform Futurwise, he doesn’t just talk about AI and the future—he lives it, inspiring audiences to take bold action. You can reach his digital twin via WhatsApp at: +1 (830) 463-6967.